Cp58 Income Tax Malaysia

Form Cp 58 Duty To Furnish Particulars Of Payment Made To An Agent Dealer Or Distributor Etc Malaysian Taxation 101

Cp 58 Malaysian Taxation 101

Cp58 Form Fill Online Printable Fillable Blank Pdffiller

Action Required Form Cp58 Year 2018 For Doterra Business Malaysia Facebook

Cp 58 Form Lhdn

What Is Cp58 Sql Account Payroll Best Payroll Software Malaysia

Deduction of expenses capital allowance 4.

Cp58 income tax malaysia. Nevertheless if the tax office requires the detail information on the rewards or incentives paid to the agents dealers or distributors the payer company must provide all the incentive information for the tax office including those rewards which are worth less than rm5 000. With effect u001efrom 1st january 2012 the new section 83a of the income tax act 1967 ita 1967 imposes the responsibility to companies to issue a form cp 58 on any incentives whether in monetary form or otherwise to its agents dealers or distributors. The appeal has been raised by tax agents and associations representing agents dealers or distributors.

Statement of incentive payment. Section 4 a business income 3. Under section 34b of the income tax act 1967. The malaysian government introduced mtd as a final tax effective from tax year 2014 and where the employee elects for mtd as a final tax will waive the requirement of filing an income tax return.

S4 a 或 s4 f 1. Mtd is only due on employment income. Income that is attributable to a place of business as defined in malaysia is. I am malaysia working and file income tax return in singapore.

Claim for special provisions single deduction under subsection 34 7 of the income tax act 1967. The mtd as a final tax option is however only open to a taxpayer who. Lim reply 我去年在两间公司打工 有两份收入. Form cp58 is unlike other tax filing form it is not required to be submitted to irbm which is why the payer company tend to ignore from preparing cp58 or they might not even know the existence of cp58.

Form cp 58 duty to furnish particulars of payment made to an agent dealer or distributor etc. The cp58 is a statement of monetary and non monetary incentive payment to an agent dealer or distributor pursuant to section 83a of the income tax act 1967. With effect u001efrom 1st january 2012 the new section 83a of the income tax act 1967 ita 1967 imposes the responsibility to companies to issue a form cp 58 on any incentives whether continue reading. I has only employment income.

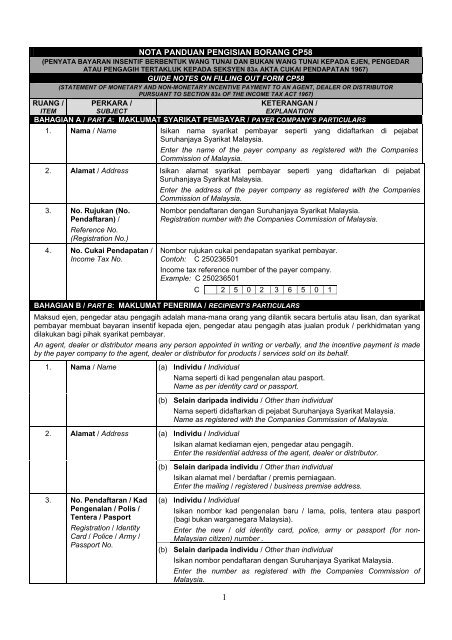

1 2017 penyata bayaran insentif berbentuk wang tunai dan bukan wang tunai kepada ejen pengedar atau pengagih tertakluk kepada seksyen 83a akta cukai pendapatan 1967 statement of monetary and non monetary incentive payment to an agent dealer or distributor pursuant to section 83 a of the income tax act 1967. The retrospective effect of the law has caused difficulties to many companies as their information systems may not have such information in the year 2011.

Cp58

Myth Of Cp58 Cheng Co

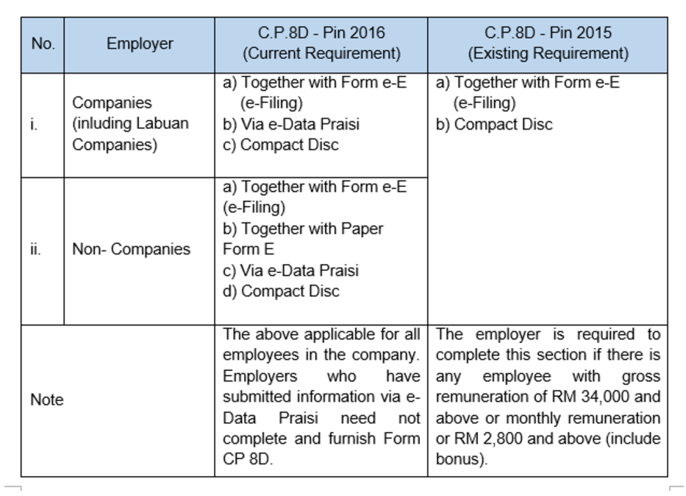

Form E Submission In 2017

Nota Panduan Pengisian Borang Cp58

Ktp Company Plt Audit Tax Accountancy Sst In Johor Bahru

Toneexcel Online Marketer Bina Pendapatan Pasif Dengan Handphone

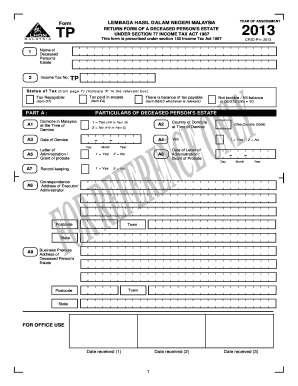

Borang Cp58 2013

Your Tax Obligation As An Employer Anc Group

Stay Home And Earn

Garis Panduan Pengemukaan Maklumat Cp58 Lembaga Hasil

.png)

Zul Rafique Partners

Ktp Company Plt Audit Tax Accountancy Sst In Johor Bahru

Https Www2 Deloitte Com Content Dam Deloitte My Documents Tax My Tax Espresso Mac2020 Special Alert Irbm Pdf

Infinitus Notice Income Tax E Statement Attention To Facebook

Dear All Fellow Members Please Remember Naturally Plus Malaysia Sdn Bhd Official Facebook

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcthjsaeyyenaz4qq0wwz4r8tvnhgk4b9 Jc Oqgqpetx7xezqvs Usqp Cau

Tp1 Form Tp2 Form Tp3 Form Malaysia Free Download Sql Payroll Hq

Qne Malaysia Sql Accounting Software Accounting System Software

Https Www Yycadvisors Com 2020 09 11t08 38 29 000000z 1 0 Https Www Yycadvisors Com Images Sme 01 Png Https Www Yycadvisors Com 2020 Second Stimulus Package Highlights Cn Html 2020 04 06t07 01 56 000000z 0 5 Https Www Yycadvisors